As we step into 2024, many Filipinos are keenly aware of the importance of healthcare coverage, especially with the rising costs of medical services. The Philippine Health Insurance Corporation (PhilHealth) plays a crucial role in providing accessible healthcare to citizens through its contributions. Understanding the changes and updates to PhilHealth contributions for 2024 and 2025 is essential for both employees and employers alike.

MANILA, Philippines — On January 12, the Philippine Health Insurance Corporation (PhilHealth) announced an important decision affecting many Filipinos: a scheduled increase in member contributions for 2024. The premium rate is set to rise from the current 4% to 5%, and this adjustment will undoubtedly impact households across the country.

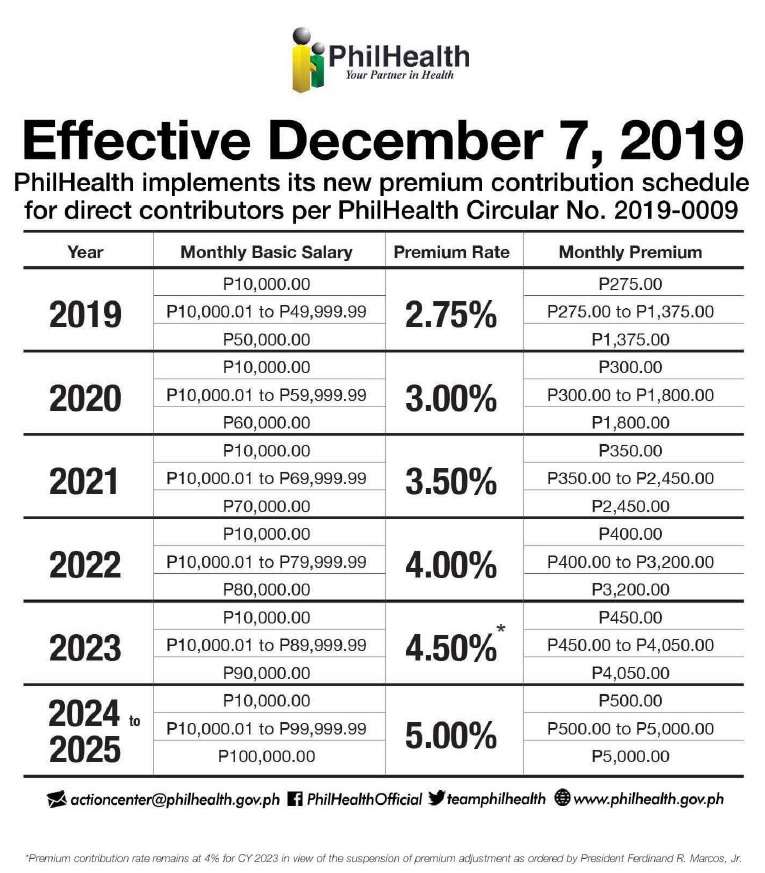

Understanding the New 5% Contribution Rate

1. New Contribution Rate for 2024

This adjustment aims to enhance the sustainability of the PhilHealth system and ensure that members receive adequate health coverage.

- Summary of the 2024 Rates:

- New Rate: 5% of the monthly salary

- Implementation Date: January 1, 2024

2. Contribution Rate for 2025

The contribution rate will remain at 5% in 2025, with further adjustments in income brackets to reflect any increases in the minimum wage and other economic factors. This stability in rates allows members to better anticipate their contributions in the coming year.

- Summary of the 2025 Rates:

- Rate: 5% of the monthly salary

- Implementation Date: January 1, 2025

Why the Increase?

The rise to 5% is not merely a number; it reflects the growing costs of healthcare in the Philippines. As medical expenses continue to rise, PhilHealth must adjust its funding to provide adequate coverage for its members. This increase aims to:

- Enhance Healthcare Services: By increasing the contribution rate, PhilHealth can provide better services, cover more medical expenses, and support various health initiatives.

- Sustain the Fund: The adjustment is necessary to sustain the health insurance fund amid increasing claims and healthcare demands.

Adjustments to the Income Range

With the implementation of the new contribution rate, PhilHealth has also made adjustments to the income brackets used for calculating contributions. This change is significant because it affects how much both employers and employees need to contribute monthly.

Revised Income Brackets

Along with the contribution rate increase, PhilHealth has also revised the income brackets that determine how contributions are calculated. Here’s a breakdown of the new brackets:

Note: This table outlines the monthly contributions according to various income brackets. It’s important to note that the contribution calculations for the income range of ₱10,001 to ₱39,999 may differ based on a specific percentage established by PhilHealth. These modifications help ensure that contributions correspond to employees’ income levels, fostering fairness and precision in the contribution process.

Example Calculation for 2024

If an employee has a monthly salary of ₱25,000, their contribution will be calculated as follows:

- Monthly Contribution

Contribution = Monthly Salary × Contribution Rate

Contribution = ₱25,000 × 0.05 = ₱1,250

Who Needs PhilHealth?

PhilHealth, or the Philippine Health Insurance Corporation, plays a crucial role in ensuring that all Filipinos have access to healthcare services. Understanding who needs PhilHealth is essential for promoting health security and financial protection for individuals and families. Here’s a breakdown of who should consider enrolling in PhilHealth:

1. Employed Individuals

- Formal Sector Workers: Employees in the private and public sectors are required to enroll in PhilHealth. Contributions are typically deducted from their salaries, and employers also contribute to their coverage.

- Casual and Contractual Employees: Even those employed on a contractual or casual basis should be enrolled, ensuring they have access to health services during their employment.

2. Self-Employed Individuals

- Freelancers and Entrepreneurs: Self-employed individuals, including freelancers and business owners, should voluntarily enroll in PhilHealth. This provides them with health coverage despite not having an employer to contribute on their behalf.

3. Overseas Filipino Workers (OFWs)

- Workers Abroad: OFWs are encouraged to enroll in PhilHealth to maintain health coverage while working overseas. This ensures they have access to healthcare services upon returning home.

4. Dependents

- Family Members: PhilHealth coverage extends to dependents of enrolled members, including spouses, children, and, in some cases, parents. Enrolling dependents helps ensure the entire family has access to healthcare services.

5. Senior Citizens

- Retirees: Senior citizens aged 60 and above are entitled to PhilHealth benefits. They should ensure their membership is active to access various healthcare services without significant financial burden.

6. Minimum Wage Earners

- Low-Income Workers: Minimum wage earners are mandated to enroll in PhilHealth, with contributions often subsidized by the government. This provides them with vital health coverage at a minimal cost.

7. Individuals with Pre-existing Conditions

- Chronic Illness Management: Those with chronic illnesses or pre-existing health conditions benefit significantly from PhilHealth coverage, as it helps manage ongoing medical expenses.

8. Unemployed Individuals

- Access to Health Services: Unemployed individuals can still enroll in PhilHealth as voluntary members. This ensures that they have access to healthcare services during times of joblessness.

Benefits of PhilHealth Membership

Despite the increased contributions, PhilHealth membership offers numerous benefits that can significantly ease the financial burden during medical emergencies. Here are some key advantages of being a PhilHealth member:

- Access to In-Patient Care: PhilHealth provides coverage for hospital stays, surgical procedures, and other in-patient services, which can save you thousands of pesos during health crises.

- Out-Patient Benefits: Members also enjoy coverage for out-patient services, including consultations with doctors, laboratory tests, and diagnostic services.

- Maternity Care: PhilHealth offers maternity benefits for members, covering pre-natal check-ups, delivery, and post-natal care, ensuring that mothers and their newborns receive the necessary healthcare services.

- Preventive Care: Regular check-ups and preventive health services are also included, promoting overall wellness and helping members catch health issues early.

To learn more about how PhilHealth membership can benefit you and how to navigate the 2024 and 2025 contribution changes, check out this guide to PhilHealth benefits.

Implications for Employers and Employees

For Employers

- Increased Payroll Costs: Employers will need to adjust their budgets to accommodate the higher contributions. This could impact overall compensation packages and operational costs.

- Compliance with Regulations: Businesses must ensure they remain compliant with PhilHealth regulations to avoid penalties. Understanding the new structure will be critical in accurate reporting and remittance.

- Employee Communication: Employers should proactively communicate these changes to their employees, explaining how the adjustments affect their contributions and the benefits they will continue to receive.

For Employees

- Budget Adjustments: Employees may need to reassess their monthly budgets to account for the increased contributions. Understanding the new rates will help them plan accordingly.

- Understanding Benefits: Employees should take this opportunity to familiarize themselves with the benefits associated with their contributions. Access to better healthcare services justifies the increase in premiums.

- Utilizing PhilHealth Services: As contributions rise, employees should ensure they maximize their PhilHealth benefits. Regular check-ups and preventive care are vital for health management.

Let’s embrace this change as an opportunity to enhance our health security and support a system that serves us all. If you have further questions or need assistance regarding your PhilHealth membership, don’t hesitate to reach out to your local PhilHealth office or visit their official website for more information.

… and you might just need our assistance.

Do you have questions about your PhilHealth membership? Set up a consultation with FilePino today! Call us at (02) 8478-5826 (landline) and 0917 892 2337 (mobile) or send an email to info@filepino.com.

One Response

this is so unfair for those not regular employee for they have no employer-employee relationship for they have no benefits such as regular employee, they are shouldering the 5% contribution for PHIC that supposed to be much lesser compared to those regular employee who earned the same salary wages, and this is not well implemented to privates sector individuals for they are the one who paid ther own contribution and yet not directly deducted into their salary, just try to see the imbalance implementation if this memorandum circular.it is NOT FAIR… INDIVIDUAL/SELF CONTRIBUTION IS THE ONE SHOULDERED THOSE CONTRIBUTION ON INDIGENT AND NHTS SECTOR